At a concession stand at Staples Center in Los Angeles, Adelaide Avila was pingponging between pouring beers, wiping down counters and taking out the trash. Her Los Angeles Lakers were playing their hometown rival, the Clippers, but Avila was working too hard to follow the March 2019 game.

When she filed taxes for her previous year’s labors at the arena and her second job driving for Uber, the 50-year-old Avila reported making $44,810. The federal government took a 14.1% cut.

On the court that night, the players were also hard at work. None more so than LeBron James. The Lakers star was suffering through a painful strained groin injury, but he still put up more points and played more minutes than any other player.

In his tax return, James reported making $124 million in 2018. He paid a federal income tax rate of 35.9%. Not surprisingly, it was more than double the rate paid by Avila.

The wealthiest person in the building that night, in all likelihood, was Steve Ballmer, owner of the Clippers. The evening was decidedly less arduous for the billionaire former CEO of Microsoft. He sat courtside, in a pink dress shirt and slacks, surrounded by friends. His legs were outstretched, his shoes almost touching the sideline.

Ballmer had reason to smile: His Clippers won. But even if they hadn’t, his ownership of the team was reaping him massive tax benefits.

For the prior year, Ballmer reported making $656 million. The dollar figure he paid in taxes was large, $78 million; but as a percentage of what he made, it was tiny. Records reviewed by ProPublica show his federal income tax rate was just 12%.

That’s a third of the rate James paid, even though Ballmer made five times as much as the superstar player. Ballmer’s rate was also lower than Avila’s — even though Ballmer’s income was almost 15,000 times greater than the concession worker’s.

Ballmer pays such a low rate, in part, because of a provision of the U.S. tax code. When someone buys a business, they’re often able to deduct almost the entire sale price against their income during the ensuing years. That allows them to pay less in taxes. The underlying logic is that the purchase price was composed of assets — buildings, equipment, patents and more — that degrade over time and should be counted as expenses.

But in few industries is that tax treatment more detached from economic reality than in professional sports. Teams’ most valuable assets, such as TV deals and player contracts, are virtually guaranteed to regenerate because sports franchises are essentially monopolies. There’s little risk that players will stop playing for Ballmer’s Clippers or that TV stations will stop airing their games. But Ballmer still gets to deduct the value of those assets over time, almost $2 billion in all, from his taxable income.

This allows Ballmer to perform a kind of financial magic trick. If he profits from the Clippers, he can — legally — inform the IRS that he is losing money, thus saving vast sums on his taxes. If the Clippers are unprofitable in a given year, he can tell the IRS he’s losing vastly more.

Glimpses of the Clippers’ real-world financial results show the business has often been profitable. Those include audited financials disclosed in a Bank of America report just before Ballmer bought the team, as well as NBA records that were leaked after he became owner.

But IRS records obtained by ProPublica show the Clippers have reported $700 million in losses for tax purposes in recent years. Not only does Ballmer not have to pay tax on any real-world Clippers profits, he can use the tax write-off to offset his other income.

Ballmer isn’t alone. ProPublica reviewed tax information for dozens of team owners across the four largest American pro sports leagues. Owners frequently report incomes for their teams that are millions below their real-world earnings, according to the tax records, previously leaked team financial records and interviews with experts.

They include Shahid Khan, an automotive tycoon who made use of at least $79 million in losses from a stake in the Jacksonville Jaguars even as his football team has consistently been projected to bring in millions a year. And Leonard Wilf, a New Jersey real estate developer who owns the Minnesota Vikings with family members, has taken $66 million in losses from his minority stake in the team.

In a statement, Khan responded: “We’re a nation of laws. U.S. Congress passes them. In the case of tax laws, the IRS applies and enforces the regulations, which are absolute. We simply and fully comply with those very IRS regulations.” Wilf didn’t respond to questions.

Ballmer’s spokesperson declined to answer specific questions, but said “Steve has always paid the taxes he owes, and has publicly noted that he would personally be fine with paying more.”

These revelations are part of what ProPublica has unearthed in a trove of tax information for the wealthiest Americans. ProPublica has already revealed that billionaires are paying shockingly little to the government by avoiding the types of income that can be taxed.

The records also show how some of the richest people on the planet use their membership in the exclusive club of pro sports team owners to further lower their tax bills.

The records upend conventional wisdom about how taxation works in America. Billionaire owners are consistently paying lower tax rates than their millionaire players — and often lower even than the rates paid by the workers who staff their stadiums. The massive reductions on personal tax bills that owners glean from their teams come on top of the much-criticized subsidies the teams get from local governments for new stadiums and further deplete federal coffers that fund everything from the military to medical research to food stamps and other safety net programs.

The history of team ownership as a way to avoid taxes goes back almost a century. Bill Veeck, owner of the Cleveland Indians in the 1940s and later the Chicago White Sox, stated it plainly in his memoir: “Look, we play the Star Spangled Banner before every game. You want us to pay income taxes too?”

Veeck is credited with convincing the IRS to accept a tax maneuver even he described as a “gimmick.” Player salaries were already treated as a deductible business expense for a team. That was not controversial in the slightest.

But Veeck dreamed up an innovation, a way to get a second tax deduction for the same players: depreciation. The way he accomplished this was by separately buying the contracts before the old company was liquidated, instead of transferring them to the new company as had been done before. That meant that the contracts were treated as a separate asset. The value a new owner assigned to that asset when he bought the team could be used to offset taxes on team profits, as well as any other income he might have. (Defenders of the practice contend that it’s not double-dipping since the deductions are taken against two separate pools of money: the money used to purchase the team and the day-to-day operating budget.)

Team owners, Veeck wrote in his memoir, had won “a tax write-off that could have been figured out by a Texas oilman. It wasn’t figured out by a Texas oilman. It was figured out by a Chicago hustler. Me.”

Once the IRS accepted this premise, the natural next step — owners assigning as large a portion of the total team purchase price as possible to player contracts — was elevated into a sport of its own. Decades ago, Paul Beeston, who was president of the Toronto Blue Jays and president of Major League Baseball at various times, famously described the result: “Under generally accepted accounting principles, I could turn a $4 million profit into a $2 million loss and I could get every national accounting firm to agree with me.”

The depreciation of tangible assets, and their decay over time, is often intuitive. A machine in a factory and a fleet of cars have more obvious fair market values and life spans before business owners will have to pay to replace them. Take, for example, a newspaper business with a printing press that cost $10 million and will last for, say, 20 years. The idea of depreciation is that the newspaper owner could deduct a piece of that $10 million every year for the 20-year lifespan of the press.

But amortization, the term for depreciating nonphysical assets, was less straightforward. Sports teams are often mainly composed of these assets. Valuing and assigning a life span to a player contract or a TV deal was more subjective and thus vulnerable to aggressive tax maneuvers by team owners.

Several NBA teams claimed that more than 90% — in one case, 100% — of their value consisted of player contracts that could be written off on the owner’s taxes, according to league financials that emerged in an early 1970s congressional investigation.

By that time the IRS had begun a series of challenges of valuation methods by team owners, part of a larger fight across industries about how business owners should be allowed to write off so-called intangible assets. The tax agency insisted that companies should only be able to write off assets with a limited useful life.

In an effort to stop the endless litigation, Congress inaugurated the modern era of amortization by simplifying the rules in 1993: Under the new regime, the purchaser of a business would be allowed, over the span of 15 years, to write off more types of intangible assets. This might have been welcome news for the sports business. But Congress explicitly excluded the industry from the law.

Following lobbying by Major League Baseball, in 2004, sports teams were granted the right to use this deduction as part of a tax bill signed by President George W. Bush, himself a former part owner of the Texas Rangers. Now, team owners could write off the price they paid not just for player contracts, but also a range of other items such as TV and radio contracts and even goodwill, an amorphous accounting concept that represents the value of a business’ reputation. Altogether, those assets typically amount to 90% or more of the price paid for a team.

That means when billionaires buy teams, the law allows them to treat almost all of what they bought, including assets that don’t lose value, as deteriorating over time. A team’s franchise rights, which never expire, automatically get treated like a pharmaceutical company’s patent on a blockbuster drug, which has a finite life span. In reality, the right to operate a franchise in one of the major leagues has in the last few decades been a license to print money: In the past two decades, the average value of basketball, football, baseball and hockey teams has grown by more than 500%.

ProPublica uncovered the tax breaks used by team owners by dissecting reports sent to the IRS that capture the profit or loss of a business. Still, untangling the precise benefits can be difficult. For example, some owners hold their team stakes in companies that also had unrelated assets — a corporate nesting doll that makes it impossible to determine the losses a team produced. The examples mentioned in this article are instances in which it appears the owners did not intermingle assets and the team’s ownership structure is clear based on ProPublica’s analysis of the tax records, court documents, corporate registration data and news reports.

When Steve Ballmer offered to buy the Clippers in 2014 for a record sum, the team’s longtime owner, Donald Sterling, was taken aback.

“I’m curious about one thing,” Sterling said at a meeting later recounted by his lawyer.

“Of course, what is the question?” Ballmer responded.

Sterling proceeded: “You really have $2 billion?”

The size of the offer was impressive considering the context. In 1981, Sterling had paid $12.5 million for the club. In the three decades that followed, Sterling had become notorious for neglecting and mistreating the team. He didn’t provide a training facility for years, forcing the team to practice at the gym of a local junior college. He heckled his own players during games. After games, Sterling was said to parade friends through the locker room so they could gawk at the players’ bodies.

But even Sterling’s mismanagement couldn’t stop the Clippers’ rise in value. Players kept signing with the Clippers — drafted rookies because they typically have no other option if they want to play in the NBA and veterans because there are a finite number of teams to choose from.

TV deals also grew in value. The Clippers had little fan support, and they oscillated between being league bottom-dwellers and a middling franchise. But before Sterling sold the team, the Clippers were expected to sign a new local media deal worth two to three times more than their previous deal.

The beginning of the end of Sterling’s tenure came when he was recorded by his mistress telling her not to bring Black people to Clippers games. The NBA moved to force Sterling out. Ballmer swooped in, outbidding Oprah Winfrey and others. (ProPublica couldn’t reach Sterling for comment. His wife, Shelly, who co-owned the Clippers with him, defended their tenure in emails to ProPublica, saying they weren’t the only owners whose team didn’t own a practice facility and suggesting her husband did not heckle players. “I GUESS WHEN THERE IS NOTHING TO WRITE ABOUT WHY NOT TRY TO WRITE SOME SCUM,” she wrote.)

Ballmer, one of the richest people in the world, wasn’t just motivated by his love for basketball. He expected the team to be profitable. “It’s not a cheap price, but when you’re used to looking at tech companies with huge risk, no earnings and huge multiples, this doesn’t look like the craziest thing I’ve ever acquired,” he said at the time. “There’s much less risk. There’s real earnings in this business.”

Two years later, as the league negotiated a new contract with the players union, Ballmer portrayed the team’s finances in a much different light. “I’m a new owner and I’ve heard this is the golden age of basketball economics. You should tell our finance people that,” he told a reporter in 2016. “We’re sitting there looking at red ink, and it’s real red ink. I know, it shows up on my tax returns.”

But losses on a tax return don’t necessarily mean losses, as large or at all, in the real world.

Ballmer was acquiring a team that had skyrocketed in value over the previous decade. And there was the benefit for his taxes: He was allowed to start treating the Clippers — including those player contracts and TV deals — as if they were losing value.

From 2014 to 2018, records show Ballmer reported a total of $700 million in losses from his ownership of the Clippers, almost certainly composed mainly of paper losses from amortization.

The evidence examined by ProPublica showed the Clippers have often been profitable, though many of the glimpses into the team’s finances are from before Ballmer took over. Leaked NBA records during Ballmer’s tenure showed the Clippers in the black as recently as 2017. Audited financials disclosed in the Bank of America report just before the sale showed the team netting $14 million and $18 million in the two years before Ballmer took over, with projected growth in the future. Tax records for the pre-Ballmer era examined by ProPublica showed the team consistently making millions in profits. Forbes has also estimated the team generates millions in annual profits.

Nevertheless, Ballmer reported staggering losses from the Clippers to the IRS. Those losses allowed him to reduce the taxes he owed on the billions he has reaped from Microsoft stock sales and dividends. Owning the Clippers cut his tax bill by about $140 million in just five years, according to a ProPublica analysis.

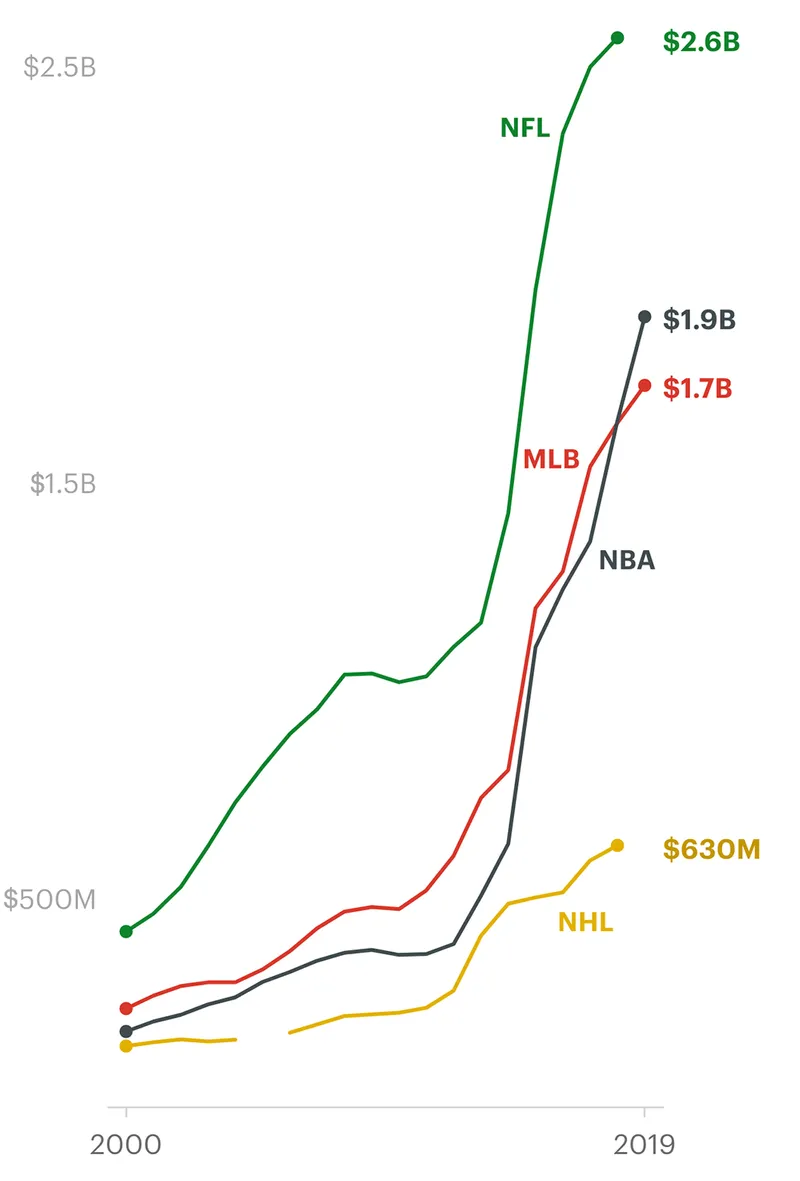

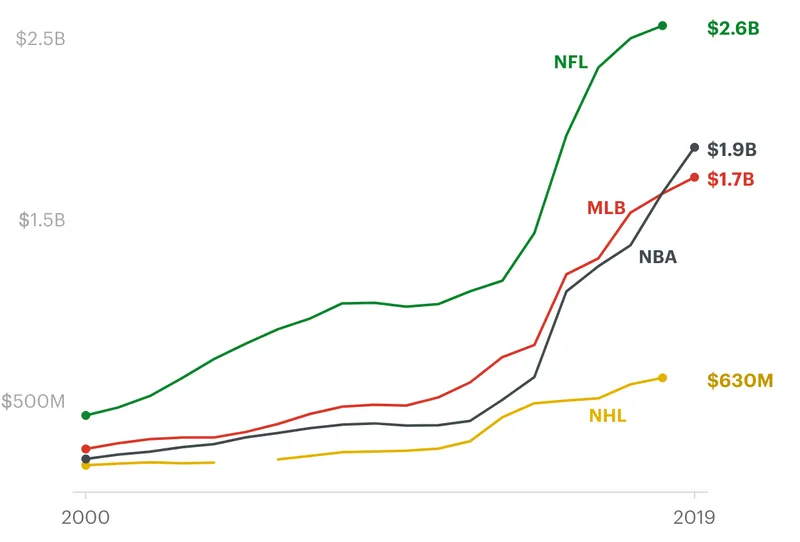

Team Values Across Professional Sports Leagues Have Increased for the Past 20 Years

On average, major sports franchises have consistently increased in value over the past two decades, according to estimates by Forbes.

Unlike billionaire team owners, millionaire players are virtually guaranteed to pay a large share of their income in taxes.

The law favors people who are rich because they own things over people who are rich because they make a high income from their work. Wages — the main source of income for most people, including athletes — are taxed at the highest rates of all, topping out at a marginal rate of 37% plus an extra 3.8% for Medicare. The government takes a smaller share of money made from, say, selling a stock. That’s not to mention the benefits available to people who own businesses, such as the paper losses created by buying a sports team.

So while Ballmer’s tax rate for 2018 was 12% on his $656 million of income, Lakers star Anthony Davis paid 40% that year on $35 million of income. Golfer Tiger Woods made $22 million and paid 34%. Boxer Floyd Mayweather paid more than 37% on his $53 million income. Star Houston Astros pitcher Justin Verlander made $30 million and paid a 39% cut.

(In each instance in which ProPublica refers to “income” in this article, we are referring to adjusted gross income, which the IRS defines as earnings minus certain items like alimony or student loan interest payments. We calculated tax rates the way government agencies and many economists do, by including not just the Medicare and Social Security taxes automatically taken out of workers’ paychecks, but also the share employers are required to pay for those programs on behalf of their employees. The rationale for including the employer’s share as part of the employee’s tax burden is that employers pay less in wages because of these costs. These levies make up most of the tax burden for the typical worker, a low but still significant percentage for millionaire players, but a negligible share or nothing for billionaires like Ballmer who typically don’t take salaries and other forms of income these taxes apply to.)

In a few cases, star players have bought pieces of pro sports teams. But that doesn’t automatically get them the low rates enjoyed by the typical billionaire owner. Basketball great Michael Jordan, for instance, owns the NBA’s Charlotte Hornets and a tiny stake in the Miami Marlins baseball team. His share of the Hornets produced $3.6 million in tax losses in 2015, even though the team was estimated to be in the black that year. He still makes a large portion of his money from Nike though, which is taxed at a high rate. That year, for example, he paid 38% in federal taxes on $114 million in income. Jordan’s spokeswoman declined to answer specific questions.

Ballmer’s tax advantages reduce the revenue flowing to the federal government. At the same time, he has publicly bemoaned the perils of having a government that spends more than it takes in. He has founded a nonprofit, USA Facts, that provides data on government spending. “Nobody wants to sacrifice anything in the short term so that we don’t leave these huge debt and deficits to our children,” he told Fox Business three years ago. “That drives me crazy.”

Perhaps the savviest tax play for billionaires interested in pro sports is buying a football team. Financial analysts believe it’s exceedingly difficult to lose money running an NFL franchise. “I think the NFL is the only sport where each team is profitable and viable,” said mining tycoon Alan Kestenbaum, now a part owner of the Atlanta Falcons, in an interview with Bloomberg.

The NFL’s TV ratings dominance, easily surpassing the NBA and other major leagues, is at the center of the sport’s money machine. Each of the 32 teams — from the small-market Buffalo Bills to the behemoth Dallas Cowboys — takes an equal share of national revenue, mostly derived from broadcasting deals. In 2019 alone those deals generated $9.5 billion, divided into $296 million slices for each team. The league recently re-upped its contracts with the networks and added Amazon’s Prime Video streaming service in an 11-year, $105 billion deal. On the expense side of the ledger, the biggest line item, player salaries, is limited since the league enforces what’s known as a hard salary cap.

Those two sources of profitability drove the record $2.3 billion price of the last NFL team to change hands, the Carolina Panthers. But the sale triggered a dramatic swing in how the team’s finances were reported to the IRS, records show. The Panthers suddenly went from producing large profits to suffering major losses.

The Panthers were built into a thriving business by Jerry Richardson, a onetime NFL player turned fast food restaurant magnate, who was awarded the expansion franchise in the early 1990s. In addition to its share of the league’s national TV deals, the team quickly built up another major revenue source, selling out virtually every game to an enthusiastic local fan base in Charlotte. Success followed on the field. By 2016, led by MVP quarterback Cam Newton, the Panthers won the NFC Championship and made the Super Bowl.

With the amortization benefit from the early years of the team used up, the Panthers produced millions of profits every year, with margins growing annually in the five years through 2017, tax records of Richardson and several previous minority owners show. ProPublica estimated the team’s annual income based on the tax information of a complex web of team entities, as well as leaked financial statements published by Deadspin.

That year, after Richardson was at the center of a lurid racism and sexual harassment scandal, he announced he was putting the team on the auction block. Several billionaires put in bids.

The winning bidder was David Tepper, founder of the hedge fund Appaloosa Management. Tepper, who made his fortune trading distressed debt and once hired Ashlee Simpson to play his daughter’s bat mitzvah, is now the league’s richest owner.

The $2.3 billion Tepper paid would produce amortization expenses of around $140 million per year, according to the IRS’ general guidelines. That annual expense would wipe out any Panthers profits for tax purposes.

The team swung from a large taxable profit before its sale to a tax loss of about $115 million, according to a ProPublica analysis of IRS records, after Tepper’s purchase in 2018. There’s no evidence anything significant about the Panthers’ real-world revenue and expenses changed between 2017 and 2018. The only major difference is the team changed hands, and Tepper now gets a tax benefit through his new entity, Tepper Sports Holdings.

Tepper’s hedge fund is a massive producer of capital gains income — in the past decade, he has often reported more than $1 billion in annual income — so the tax losses produced by the Panthers are extremely valuable to him. A spokesman for Tepper didn’t respond to questions.

The same year Tepper bought the Panthers, the NHL’s newest hockey team, the Las Vegas Golden Knights, accomplished what only one expansion team had done before by making it to the league finals in its inaugural season. Since then, the Golden Knights have continued to win. Off the ice, they’ve been among the best in the NHL at motivating fans to spend money on team apparel, and the Golden Knights have consistently sold out their home games.

The team’s owner, William Foley, the chairman of insurance giant Fidelity National Financial, made it clear he wasn’t in the business of losing money. “We developed a conservative business plan,” Foley told a reporter in 2017, the first year the team played. “I didn’t want to write $20 million checks every year.” He likely didn’t have to. Forbes estimated millions in profit for the team from 2017 to 2019.

But for tax purposes, records show, the team produced losses of more than $57 million during those years. That was thanks in part to the team’s ability to write off the $500 million expansion fee that Foley paid to the NHL in 2016.

In a statement to ProPublica, Golden Knights Chief Legal Officer Peter Sadowski did not respond to questions about amortization. He did respond to a question about one of the team’s income streams, noting that the money from season ticket deposits was “used to pay rent, to employ hundreds of people, provide outstanding entertainment and create a source of pride for our community.”

The Golden Knights’ tax losses helped offset the money Foley made from his other ventures, saving him more than $12 million in taxes over two years, according to a ProPublica analysis.

The value of sports franchises, as noted, tends to rise inexorably — but teams sometimes lose money along the way. Internal NBA records obtained by ESPN in 2017 showed that the league’s clubs were averaging almost $18 million in net income that season. But nine of the 30 clubs were in the red.

Even when a team spends more than it takes in, an owner can still end up on top. The amortization benefit can turn a loss into an even larger loss, which can then be used to offset other income and save money on taxes.

For example, Dan Gilbert, founder of Quicken Loans, was able to lower his taxable income by about $443 million from 2005 to 2018 because of his stake in the Cleveland Cavaliers, tax records show. In that same period, the team reached the pinnacle, winning its first-ever NBA championship in 2016.

In emails to ProPublica, Gilbert’s lawyer wrote that the team consistently loses money. “During the entire time after Mr. Gilbert’s purchase of the team, the Cavaliers has operated with an actual loss (negative cash flow/negative income) unrelated to any depreciation or amortization and there have been no funds to distribute to Mr. Gilbert or any other owner,” he wrote.

The tax write-off for amortization, Gilbert’s lawyer argued, is essential to all businesses, from restaurants to factories to sports franchises. Without it, he wrote, “there would be no capital investments made by owners and businesses would be taxed on revenue without properly taking into account all costs necessary to generate that revenue. That would be antithetical to capitalism and fatal to the United States’ economy.”

Gilbert’s lawyer added that the Cavaliers owner has paid “enormous” taxes for many years. He also wrote: “Your e-mail makes reference to other wage earners such as the players and their salaries. The facts are this: Mr. Gilbert is the only party referenced in your e-mail who has undertaken any risk. Mr. Gilbert has risked the purchase price paid for the Cavaliers, his subsequent capital contributions, the debt he has personally guaranteed and the players’ salaries which are guaranteed. ... To compare the guaranteed salaries of the Cavaliers’ players as an applicable measure of Mr. Gilbert’s tax rate is absurd.”

Advocates for team owners point out that when owners sell their teams, they have to pay back the taxes they avoided by using amortization. But even if owners ultimately repay the taxes they skipped, deferring payment of those taxes for years, sometimes decades, essentially amounts to an interest-free loan from taxpayers. An owner could reap huge gains by investing that money.

If owners die while holding their stake, as many do, the tax savings may never be repaid. And their heirs can generally restart the amortization cycle anew.

Bob Piccinini was a minority member of the group that purchased the Golden State Warriors in 2010. He made his fortune turning Modesto-based Save Mart Supermarkets into the largest family-owned grocery chain in California. Already a part owner of multiple baseball teams, he entered the basketball world not because he had a particularly keen interest in the sport, but to make money. “Sports franchises continue to go up in value,” Piccinini said at the time.

His tax information shows he bought more than 7% of the Warriors. From 2011 to 2014, he reported total losses of $16 million. Nearly a decade’s worth of tax data from other Warriors owners, also reviewed by ProPublica, showed many millions in losses — all of it during a period when the team rose to become historically dominant. Meanwhile, leaked financials obtained by ESPN from 2017 show the Warriors to be an extremely profitable business, netting $92 million in one season alone. Forbes estimates also put the team well in the black during that period. A Warriors spokesperson declined to answer a series of specific questions, instead providing a one-sentence statement: “Over the course of the last decade, we have invested hundreds of millions of dollars into our team on the court, our overall operation and, of course, the construction and opening of a new, 100 percent privately financed arena in San Francisco.”

Piccinini died in 2015. The court records about the inheritance he left his children don’t specifically mention his stake in the team or whether his estate paid taxes following his death. But the tax code likely would have allowed his children never to repay the government for the paper losses their father enjoyed. It would also have permitted Piccinni’s heirs to begin claiming paper losses of their own.

In the years since, Piccinini’s son, Dominic, has been a courtside regular at Warriors games. An occasional actor in his 20s, Dominic has an Instagram profile that shows him high-fiving Stephen Curry and other players midgame and posing for photos with rappers including Drake and E-40. In 2019, he and a friend went viral when ESPN panned to them drinking from golden chalices.

In an interview, Dominic told ProPublica that he allowed his family’s lawyers to handle the tax details of his inheritance, which granted him and his siblings equal shares of their father’s stake in the Warriors.

“It’s just the darndest thing,” he said in a phone call from a vacation in Mexico. “I’m a lucky son of a bitch, there’s no way around it.”

Additional image credits: Anthony Davis (Zhong Zhi/Getty Images), Daniel DeVos (Lev Radin/Pacific Press/LightRocket via Getty Images), Floyd Mayweather (Ethan Miller/Getty Images), John Henry (Chris Brunskill/Fantasista/Getty Images), Josh Harris (Andy Marlin/Getty Images), Justin Verlander (Jason Miller/Getty Images), LeBron James (Ethan Miller/Getty Images), Philip Anschutz (Taylor Hill/FilmMagic),Stan Kroenke (Brandon Williams/Getty Images), Steve Ballmer (Allen Berezovsky/Getty Images), Tiger Woods (Ezra Shaw/Getty Images)