This story was co-published with the Los Angeles Times and also appears in that newspaperâs Nov. 11, 2008 issue.

Goldman, Sachs & Co. urged some of its big clients to place investment bets against California bonds this year despite having collected millions of dollars in fees to help the state sell some of those same bonds.

The giant investment firm did not inform the office of California Treasurer Bill Lockyer that it was proposing a way for investment clients to profit from California's deepening financial misery. In Sacramento, officials said they were concerned that Goldman's strategy could raise the interest rate the state would have to pay to borrow money, thus harming taxpayers.

"It could exaggerate people's worries about our credit," said Paul Rosenstiel, head of the public finance division of the treasurer's office.

Such worries would tend to drive down the price of California bonds. That, in turn, would drive up the interest rate the state and its municipalities pay to borrow money. An increase of a single percentage point on a $1-billion bond issue would cost taxpayers an additional $10 million a year in interest.

That's especially troublesome at a time of severe budget turmoil and tight credit. Gov. Arnold Schwarzenegger has warned that the state could run out of cash as early as February.

Some experts said the investment bank's actions, while not illegal, might be inappropriate. "That's not a good way to do business," said Geoffrey M. Heal, professor of public policy and business responsibility at Columbia University. "They've got a conflict of interest and they're acting against the interest of their customers. . . . You act in the interests of your clients. You don't screw them, to put it bluntly."

Goldman declined to discuss the details of its trading strategy. "We continue to support our clients and underwrite transactions," spokesman Michael DuVally said in an e-mail response to written questions on Oct. 28. He said Goldman "as a firm" was no longer giving the trading advice to clients. He declined to elaborate.

Goldman's strategy was embodied in a 58-page report presented to institutional investors in September. The document, stamped "Proprietary and Confidential," was obtained by ProPublica, a New York-based nonprofit organization specializing in investigative reporting. This article was reported jointly by ProPublica and the Los Angeles Times.

Goldman stood to profit from several aspects of California's borrowing, which involves the sale of bonds to investors. First, it collected millions of dollars in fees for bringing the bonds to market and finding buyers. Then it marketed a financial instrument known as a credit default swap that is essentially an insurance policy against a bond default.

The bond investor buying the instrument pays a fee in exchange for a promise of a full refund of the bond's face value should a state such as California abruptly refuse to pay back what it owes. Such defaults are extremely rare -- California, for example, has never defaulted -- but the swaps' prices rise as states or municipalities slide into tough times economically.

Goldman, according to sources familiar with municipal bond trading, has been a leading dealer in municipal credit default swaps. The New York-based firm was trying to expand that niche market into one with broader appeal to major investors.

The company also is an important underwriter of California municipal securities. Over the last five years, it has earned about $25 million in underwriting fees from California issues.

The 58-page document advised big investors how they could profit from -- or hedge against losses in -- financial markets that had become extremely volatile and unpredictable. The firm advised "shorting" -- that is, betting on a price decline -- in markets for corporate junk bonds, European banks, the euro and British pound currencies, and U.S. municipal bonds.

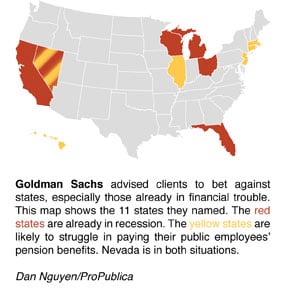

Several large states, including California, faced "worsening fiscal outlooks," the report said. It cited the recent bankruptcy of the Bay Area city of Vallejo as evidence of the "worsening fundamentals of municipal finances."

Meanwhile, muni bond insurers were suffering credit downgrades, it noted, which undermined the quality, and therefore the prices, of the bonds they had insured. And the credit crunch was forcing big investors such as hedge funds to dump their muni bond portfolios, driving down the bonds' prices.

Goldman recommended making the short bets via credit default swaps, a market in which it played a major role.

These instruments are designed to allow investors and speculators to hedge, or insure against, the risk that bond issuers or other debtors might default on their obligations. In their customary form, they are contracts that require their sellers -- in this case Goldman Sachs -- to buy back from a swap holder a defaulted bond at 100 cents on the dollar, thus insuring against any loss.

In that way, the swaps could be beneficial to the market, encouraging risk-averse investors to buy more municipal bonds. But like derivative securities in general, they can be dangerous to hold. That's because they are often highly leveraged. A small investment can buy coverage on bonds worth much more. If defaults rise to unexpected levels, the swap sellers could be hard-pressed to make good on their promises.

The perils of the credit default swap market were brought home this year, when they were instrumental in the collapse of Lehman Bros. Holdings, American International Group and Bear Stearns. Lehman and AIG were rumored to owe far more than they could pay on swaps they had sold. Meanwhile, the prices of default swaps on the three firms soared, signaling to investors that the firms might be in trouble. Investigations continue into whether those swaps may have been manipulated to undermine confidence in the firms and drive them out of business.

"By encouraging people to buy swaps, you're pushing up the price of those and making it more expensive to insure against the default on the bond that you're buying," Heal said. "The fact that such coverage has gone up in price will signal to the investor that the riskiness of the bond has increased, even if that's not true. Even if the underlying financial situation of the state has not, in fact, changed."

Indeed, what some traders found perplexing about the push for a market in municipal credit default swaps was that muni defaults almost never happen.

Goldman was a leader in the effort to build up the market for the muni swaps. In May, when the financial information firm Markit introduced a municipal CDS index to give swap traders a benchmark to set prices, Goldman was listed as one of the seven dealers participating in the rollout.

For some time before that, Lockyer told The Times, Goldman had "regularly urged" California to trade in the municipal swaps itself, ostensibly to hedge the state's risks as a bond issuer. Lockyer refused.

The trading strategy that Goldman pitched to institutional investors was apparently crafted in the spring and summer. The company may have hoped to parlay the swaps market into more activity in municipal bond trading, which is traditionally light because muni investors tend to hold the bonds to maturity.

Theoretically, the swaps index could lure speculators into the muni market, a development that would create much more fluctuation in daily prices, which in turn would generate revenue for trading desks at Goldman and other investment firms.

Lockyer and Rosenstiel said they became aware of the introduction of the muni swaps index but had not detected an effect on trading or pricing of California bonds.

But they also said the market was so complex, and the conditions affecting municipal bond prices so numerous, that it might be difficult to identify any specific cause for a given price change in California debt issues.

"The existence of the credit default swap market in muni bonds has the potential to hurt muni issuers," Rosenstiel said, "but it also has the potential to help muni issuers, and I don't think we have enough experience to know which is which."

He acknowledged that it was not unusual for a full-service investment firm such as Goldman Sachs to have to navigate among potential conflicts of interest.

"Investment banks bring issuers and investors together," he said. "Securities law has recognized the potential for a conflict of interest in playing both roles."

Under the law, the solution is for the parts of the firm dealing with either side to be isolated from each other so that information does not improperly flow between them to benefit one set of clients more than another. There is no evidence that the wall was breached in this case. Assuming such protection was in place, Lockyer said that fear of market manipulation was unfounded.

Still, Heal said he was surprised by Goldman's actions. "Goldman Sachs has a reputation as behaving in a responsible manner . . . and I don't think this is consistent with their traditions," he said.

"States are going to have to cut back on education, social services, a whole range of things because of the lack of credit. This is not just a Wall Street thing. This is going to affect the lives of less affluent people in the states that are affected."

In any case, there are signs that the muni swap index has been a bust. Tom Graff, managing director of Baltimore-based Cavanaugh Capital Management, said that by the end of August the index had failed to attract much business. It was destined "for oblivion," he said, in part because muni defaults were so rare.

Lifsher, a Times staff writer, reported from Sacramento, and staff writer Hiltzik reported from Los Angeles.