This story was co-published with WNYC Radio.

When Patrice and Philip Morgan bought a house near the ocean

in Brooklyn, they were not particularly worried about the threat of flooding.

Federal maps showed their home was outside the area at a

high risk of flood damage. For that reason, the government did not require them

to buy flood insurance, a cost imposed on neighbors on more vulnerable blocks.

Even so, the couple decided to raise their house four feet

to protect their basement from the effects of heavy rain storms.

“We thought we might have a foot or two of water,” Patrice

said, “so we put a sump pump in to avoid any small issues.”

But the maps drawn up by the Federal Emergency Management

Agency were wrong. And government officials knew it.

According to documents and interviews, state, local and

federal officials had been aware for years that the crucial maps of flood risks

were inaccurate; some feared they understated the dangers in New York City’s

low-lying areas.

The flaws in the maps had significant impact. Developers

relied on FEMA’s assessment of risks when they built new homes near the water.

And homeowners and businesses made crucial decisions about where to buy or

lease property on the assurance that they were outside of the high-risk zones.

Thousands of the buildings incorrectly identified as outside

the flood zone were damaged when seawater surged ashore as Hurricane Sandy made

landfall on Oct. 29, 2012.

State and city officials had been asking FEMA for years to

revise the maps with technology and modeling methods that didn’t exist when they

were first drawn in the 1980s. William S. Nechamen,

New York State’s floodplain chief, warned FEMA in

a 2005 letter that the failure to do so “will lead to higher than necessary

flood damages and more expenses placed on individuals and on FEMA.”

Yet, despite Nechamen’s warning,

FEMA missed chances to make changes that could have protected city dwellers from

some of the worst of Sandy’s destruction.

During a push to modernize flood maps in the mid-2000s, FEMA

decided to save money in New York City and much of the rest of the country by

digitizing old flood maps without updating the underlying information, rather

than using new technology to create more accurate maps.

The agency changed course in 2006, but didn’t release maps with

better elevation data and more accurate storm-surge models until months after

Sandy – too late to help New Yorkers like the Morgans.

When FEMA finally released a preliminary version of those maps

this January they showed that the number of city structures considered at high risk

of flooding had doubled. More than 35,000 additional homes and businesses were added

to the map’s riskiest zones, according to a study by New

York City’s Office of Long-Term Planning and Sustainability. Some 9,503 of

those buildings suffered damaged during Sandy, a ProPublica analysis of flood

maps shows.

FEMA did not respond to specific questions about the

adequacy of its flood maps or glitches in the modernization process. Bill

McDonnell, the deputy director for mitigation for FEMA’s Region II,

acknowledged that no new data had been collected to update maps for New York or

New Jersey in the mid-2000s. In a statement, the agency said it began giving

priority to map updates for “high-risk, coastal areas” in 2009. These included

14 counties in New Jersey and New York City. The agency said it continues to

work with state and local officials to “incorporate the best available data

into maps.’’

That didn’t help the Morgans. Their

home, a 1920s bungalow to which they added a second floor, was hit hard by

Hurricane Sandy.

“The whole basement was destroyed,” said Patrice Morgan, a

professor at Kingsborough Community College who was pregnant with her third

child when Sandy arrived. “We had to rip out four feet of our walls, replace

all of our appliances.”

The family spent more than five months at Patrice’s parents’

house in Bensonhurst before they could move back in. The

Morgans received $17,000 from FEMA and $6,000 from

their homeowners’ insurance, but spent nearly $50,000 out-of-pocket to rebuild

their home.

The error in calculating the Morgans’

flood risk was substantial. The map that existed when they bought the house in

2008 predicted that floodwaters would rise less than a foot even in rare storms,

those with a 1 percent chance of occurring in any year. The new maps predict

floodwaters 11 feet deep for that block under those conditions.

Philip Orton, an oceanographer at the Stevens Institute of

Technology who worked as a technical reviewer on the new maps, said most of the

difference can be accounted for by more accurate mapping data and technology.

Rising sea levels due to climate change accounts for no more than six inches of

the increase, Orton said.

If they’d known in 2008 what they know now, Philip Morgan

said, the house’s entire layout would be different.

“Our utilities are in the basement,” he said. “We would have

moved that to a higher floor. Higher, that’s the key.”

FEMA’s sputtering effort to update its flood maps dates back

about a decade.

The maps serve several crucial functions. Beyond helping to

set standards for development in areas considered high-risk, they determine the

rates homeowners pay for insurance through the National Flood Insurance

Program. Homeowners with federally backed mortgages in high-risk flood zones

— where the annual chance of flooding is estimated at 1 percent or higher

— are required by law to purchase flood insurance.

Until 2003, FEMA had been using mostly paper maps drawn in

the 1970s and ‘80s. That year, at the urging of floodplain administrators,

Congress passed legislation allocating about $1 billion — $200 million a year for

five years — to update and digitize the nation’s flood maps.

But David Maurstad, who ran the flood

insurance program from 2004 to 2008, said he told the White House’s Office of

Management and Budget early in his tenure that the money authorized wouldn’t come

close to covering the cost of updating all the maps.

“I indicated to them that I want to make sure you understand

that this is a down payment — less than a third of the maps are going to

get new engineering,” he said.

New engineering was crucial because modern technologies are capable

of producing far more accurate maps. Lidar, which

is collected by airplanes that shoot laser pulses at the ground, can detect

differences in ground elevation of as little as 3 inches and produces data

that’s 10 times as accurate as that used to generate earlier

maps. And computer programs such as ADCIRC can model storm surge and wave action

with far greater accuracy.

“There can be massive under-predictions with the old

technology,” said Joannes Westerink,

an engineering professor at the University of Notre Dame and a co-developer of

ADCIRC, “simply because it wasn’t representing the physics right.”

But updating maps with new engineering isn’t cheap.

When FEMA started updating New York City’s maps in 2003, it

used elevation data from the old maps and matched it up with modern satellite

imagery “in order to stretch the mapping budget,” said Lisa King, a

spokeswoman for the New York State Department of Environmental Conservation.

The result: Digital maps that weren’t much more accurate

than the paper ones they replaced.

City and state officials weren’t happy.

New York City specifically requested that FEMA gather lidar data for its new maps and was rebuffed, according to

a city official who requested not be named.

“The

City had serious concerns about the accuracy of this data,” the official said

in an email to ProPublica, “and stated this in numerous meetings and then in a

formal letter to FEMA.”

Nechamen, the

state floodplain chief, called FEMA’s strategy “misguided and

counterproductive” in his 2005 letter to Maurstad at

FEMA.

“This is insufficient and will result in poor quality, but

really good looking maps that fail to provide the data needed to adequately

manage development in floodplains,” he wrote. “Many errors on existing maps

will continue to appear on the new maps.”

Nechamen

referred requests for comment to the New York State Department of Environmental

Conservation, which did not respond to requests to make him available for an

interview.

In an interview, Maurstad said he had

received similar complaints from officials from other states as well.

“This is consistent with what many of the state folks were

expressing at the time,” he said.

As a result, in 2006, FEMA changed its flooding-mapping

strategy in what it called a “midcourse

adjustment,” which

called for producing digital maps for about 92 percent of the country, rather

than the whole nation. The agency said it would use the money it saved to

increase slightly the number of areas that got new engineering.

But New York City’s flood maps didn’t get much new

engineering — not new storm-surge analyses or lidar

elevation data.

Some states saw the need for better maps as so urgent that

they took it upon themselves to gather the data. North Carolina decided to pay for

mapping the state using lidar after Hurricane Floyd

in 1999. “We were concerned at the time that FEMA didn’t have the money,” said

John Dorman, the director of the North Carolina Floodplain Mapping Program.

Other parts of New York had more accurate data than New York

City. The maps for Nassau and Suffolk counties on Long Island, finalized in

2009, had been drawn using lidar and new storm-surge

models. (Much of that data had been gathered by the Army Corps of Engineers.)

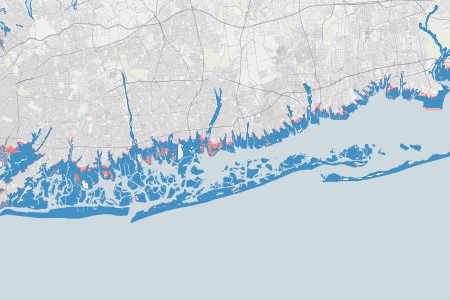

It made a huge difference when Sandy struck. According to ProPublica’s analysis, 75 percent of the flooded area in

Suffolk County and 89 percent of the flooded area in Nassau County fell within

the high-risk zones on the new maps.

No map, of course, can predict all the idiosyncrasies of a

particular storm, a FEMA specialist told ProPublica.

But maps for Brooklyn and Queens, the city’s hardest-hit

boroughs, predicted Sandy’s flooding far less reliably. Only 47 percent of the

flooded area in Brooklyn and 54 percent of the flooded area in Queens was in

the area considered high-risk. (See our interactive news

application to explore how coastal New York and New Jersey counties rank at

predicting Sandy’s surge. See

our methodology for more about how we analyzed the flood map data.)

Queens

54%

Of Sandy flood area predicted by flood maps

Kings

47%

Of Sandy flood area predicted by flood maps

Nassau

89%

Of Sandy flood area predicted by flood maps

FEMA started updating New York City’s maps again in 2009,

only two years after the previous flood maps had been released. This time they

undertook a new storm-surge analysis and included lidar

data that the city itself spent

$450,000 to gather in 2010. (The effort was partly financed with a

grant from the U.S. Department of Energy.)

But these maps weren’t ready in time for Sandy, a delay that

carried a high price.

Nearly 400 of the buildings that suffered damage during

Sandy had been built or modified since 2007, when the less-accurate maps came

out, ProPublica’s analysis showed. Those buildings weren’t

included in high-risk flood zones; now they are.

Rita Brummer poses for a portrait with her Shih Tzu, Coco Chanel, at her home in the Rockaways on Monday afternoon. In the background, a worker removes siding from the house. Brummer and Steven Farrara are still working on their home more than a year after it was flooded by Superstorm Sandy. The pair dropped their flood insurance coverage less than a year before the storm, when they were told their property did not fall into the high-risk flood zone. (Karsten Moran for ProPublica)

Rita Brummer and Steven Ferrara,

who live in the Belle Harbor neighborhood in Queens, paid flood insurance

premiums for more than 20 years before they dropped their coverage less than a

year before Sandy flooded their home. On the 2007 maps, their home wasn’t in a

high-risk flood zone.

“Nobody believed the storm was going to hit us like this,” Brummer said.

The surge of salt water and sewage that flooded their home

caused more than $100,000 in damage, much of which the couple paid to repair themselves.

On the updated maps released this year, their house was in a high-risk zone. Had

she known that sooner, Brummer said, she “never would

have dropped” her flood insurance.

More than 100 other homes that suffered damage in Belle

Harbor also did not fall into the high-risk flood zone on the old flood maps

but are considered high-risk on the maps released this year.

Those maps are in the process of being refined further. In

the weeks after the storm, FEMA rushed to release incomplete “advisory”

versions, then issued more complete updates this January.

The maps are expected to be finalized in 2015.

Imperfect as they remain, New York City’s flood maps are

more advanced than those covering some other parts of the country. Five coastal

counties in New Jersey still use paper maps dating back decades. FEMA has been in the

process of revising New Orleans’ maps since the Army Corps shored up

the city’s flood protection after Hurricane Katrina in 2005, and still

officially relies on paper maps from 1984.

Though the federal government approved more than $60 billion

in aid after Hurricane Sandy, including a $9.7 billion increase in the National

Flood Insurance Program’s borrowing limit, it has actually cut spending on

flood mapping in recent years. Congress

allocated $99 million for updating maps in 2012, roughly half of what

it had spent annually since 2004. About the same amount was allocated for this

year.

In a report released in March, the Association of State Floodplain

Managers estimated the

total cost of updating flood maps nationwide at $4.5 billion to $7.5

billion. It also estimated that the maps, even in their current state, save the

country about $1 billion a year in flood-related damages.

Chad Berginnis, the association’s

executive director, said that the absence of accurate flood maps could lead to

an “entire cascade of impacts”: higher costs to taxpayers in the form of

disaster assistance, higher likelihood of injury and death for residents, lost

tax revenue and damaged infrastructure after flooding occurs.

“All of those typical effects are things that happen when

you don’t have good, accurate flood data that you’re using,” he said.