When Donna Edgar found out that new flood maps from the Federal Emergency Management Agency would place her house in a high-risk flood zone, she couldn’t believe it.

Her home, on the ranch she and her husband own in Texas hill country about 60 miles north of Austin, sits well back from the nearby Lampasas River.

“Her house is on a hill,” said Herb Darling, the director of environmental services for Burnet County, where Edgar lives. “There’s no way it’s going to flood.”

Yet the maps, released last year, placed the Edgars in what FEMA calls a “special flood hazard area.” Homeowners in such areas are often required, and always encouraged, to buy federal flood insurance, which the Edgars did.

FEMA eventually admitted the maps were wrong. But it took Edgar half a dozen engineers (many of whom volunteered their time), almost $1,000 of her own money and what she called an “ungodly number of hours” of research and phone calls over the course of a year to prove it.

Edgars is far from alone.

From Maine to Oregon, local floodplain managers say FEMA’s recent flood maps — which dictate the premiums that 5.5 million Americans pay for flood insurance — have often been built using outdated, inaccurate data. Homeowners, in turn, have to bear the cost of fixing FEMA’s mistakes.

“It’s been a mess,” Darling said. “It’s been a headache for a lot of people.”

Joseph Young, Maine’s floodplain mapping coordinator, said his office gets calls “almost on a daily basis” from homeowners who say they’ve been mapped in high-risk flood areas in error. More often than not, he said, their complaints have merit. “There’s a lot of people who have a new map that’s unreliable,” he said.

Maps built with out-of-date data can also result in homeowners at risk of flooding not knowing the threat they face.

FEMA is currently finalizing new maps for Fargo, N.D., yet the maps don’t include any recent flood data, said April Walker, the city engineer, including from when the Red River overran its banks in 1997, 2009 and 2011. Those floods were the worst in Fargo’s history.

Fargo has more recent data, Walker said, but FEMA hasn’t incorporated it.

It’s unclear exactly how many new maps FEMA has issued in recent years are at least partly based on older data. While FEMA’s website allows anybody to look-up flood maps for their areas, the agency’s maps don’t show the age of the underlying data.

FEMA’s director of risk analysis, Doug Bellomo, said it was “very rare” for the agency to digitize the old paper flood maps without updating some of the data. “We really don’t go down the road” of simply digitizing old maps, he said.

FEMA did not respond to questions about the maps for Fargo or other specific areas.

State and local floodplain officials pointed to examples where FEMA had issued new maps based at least in part on outdated data. The reason, they said, wasn’t complicated.

“Not enough funding, pure and simple,” Young said.

Using new technology, FEMA today is able to gather far more accurate elevation data than it could in the 1970s and 1980s, when most of the old flood maps were made. Lidar, in which airplanes map terrain by firing laser pulses at the ground, can provide data that’s 10 times more accurate than the old methods.

Lidar is also expensive. Yet as we’ve reported, Congress, with the support of the White House, has actually cut map funding by more than half since 2010, from $221 million down to $100 million this year.

With limited funding, FEMA has concentrated on updating maps for the populated areas along the coasts. In rural areas, “it’s sort of a necessary evil to reissue maps with older data on them,” said Sally McConkey, an engineer with the Illinois State Water Survey at the University of Illinois at Urbana-Champaign, which has a contract with FEMA to produce flood maps in the state.

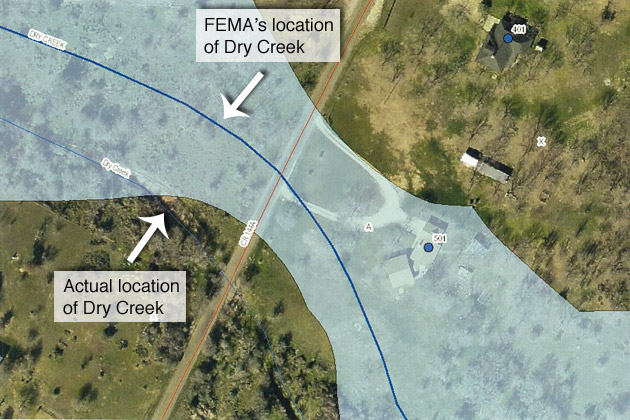

When old maps are digitized, mapmakers try to match up road intersections visible on them with the ones seen in modern satellite imagery (similar to what you can see using Google Earth). But the old maps and the new imagery don’t always line up correctly, leading to what Alan R. Lulloff, the science services program director with the Association of State Floodplain Managers, called a “warping” effect.

“It can show areas that are actually on high ground as being in the flood hazard area when they’re not,” he said. “That’s the biggest problem.”

When FEMA issued new maps last year for Livingston Parish in Louisiana, near Baton Rouge, they included new elevation data. But the flood studies, said Eddie Aydell III, the chief engineer with Alvin Fairburn in Denham Springs, La., who examined the maps, were “a conglomeration of many different ancient engineering studies” dating from the 1980s to 2001. The mapmakers did not match up the new elevation data with the older data correctly, he said, making structures in the parish seem lower than they really are.

“It’s going to be a nightmare for the residents of our parish,” he said.

Bonnie Marston’s parents, Jim and Glynda Childs, moved to Andover, Maine, where Marston lives with her husband, in 2010 with the intention of building a house. But when they applied for a loan the bank told them that FEMA’s new flood maps for the county, issued the year before, had placed the land on which they planned to build in a special flood hazard area. The cost: a $3,200 annual flood insurance bill, which the Childs had to pay upfront.

Marston spent about $1,400 to hire a surveyor, who concluded her parents did not belong in a special flood hazard area. FEMA eventually removed the requirement for them to buy flood insurance — though it didn’t actually update the map. The bank refunded the flood insurance premium, but Marston said FEMA wouldn’t refund the cost of the survey.

“In my mind it’s a huge rip-off,” Marston said.

Edgar, 68, a retired IBM software developer, said she couldn’t understand why FEMA thought her house was suddenly at risk of flooding. When she called FEMA and asked, she said the agency couldn’t tell her.

“They just said, ‘You need to buy flood insurance,’” she said, and told her she could apply for what’s known as a letter of map amendment if she thought she’d been mapped into a special flood hazard area in error. She worried that being in a high-risk flood area would diminish the value of her home.

Her husband, Thomas, a professor of chemical engineering at the University of Texas at Austin, knew David R. Maidment, a civil engineering professor there who is an expert on flood insurance mapping. While she hired a surveyor and wrangled with FEMA, Maidment and several of his Ph.D. students drove up to the ranch to study it as a class project.

The experience, Maidment said, showed him “in a very small microcosm” the importance of using up-to-date elevation data in new maps. The Texas state government paid to map Burnet County, where the Edgars’ ranch is located, in 2011 using lidar. But FEMA’s new maps for the county don’t include the lidar data.

FEMA removed the Edgars from the special flood hazard area in March, but again it hasn’t actually changed the maps. Letters of map amendment acknowledge that FEMA’s maps were incorrect without actually changing them. While the Edgars don’t have to buy flood insurance, the new, inaccurate maps remain.

Darling, the county’s director of environmental services, said he had gotten calls from dozens of homeowners with similar complaints about the new flood maps.

“We’ve still got ‘em coming in,” he said.

The contractor that created the new maps appeared to have taken shortcuts in drawing them, Darling said. Without new lidar data, he added, issuing a new map is “just a waste of money.”

The experience, Edgar said, had left her feeling deeply frustrated, as a both homeowner and a taxpayer. FEMA hasn’t reimbursed her for the surveying costs or for the flood insurance premium she and her husband paid. “It falls to the homeowner to hire a professional engineer and pay” hundreds, even thousands, “to disprove what I would call their shoddy work,” she said. “I don’t think that’s fair.”

Have you experienced problems with FEMA's flood maps firsthand? Let us know.