The big question these days is whether the government will step in and take over the nation’s faltering major banks. Details in the government’s recent agreement with Citigroup to limit the bank’s losses show how the Bush administration was haltingly moving in the direction of a takeover, but only after significant further losses at the bank.

The big question these days is whether the government will step in and take over the nation’s faltering major banks. Details in the government’s recent agreement with Citigroup to limit the bank’s losses show how the Bush administration was haltingly moving in the direction of a takeover, but only after significant further losses at the bank.

Last November, government officials intervened to halt Citigroup’s free fall. The Treasury Department ponied up $20 billion in exchange for preferred shares. That’s on top of the $25 billion pumped into Citigroup as part of the original move to bail out banks. As part of the November deal, regulators also agreed to backstop a $301 billion pool of assets by absorbing a portion of the losses beyond a certain point. (The government recently struck a similar deal with Bank of America.)

Last week, Citigroup finally released the details of that agreement in an SEC filing. It provides for government officials to dictate management of the assets should losses exceed $27 billion.

Here’s how the deal will work: $301 billion in assets are covered. Citi will absorb the first $39.5 billion in losses — this is referred to as Citi’s “deductible” in the agreement. If the losses continue past the deductible, the government will absorb 90 percent of the losses. A trio of governmental agencies would pay that share: The Treasury would first use $5 billion from the TARP, then FDIC would put up $10 billion, and a Federal Reserve loan would provide the last resort. As a fee, the Treasury and FDIC together are receiving a total of $7.06 billion of preferred stock in Citi — bringing the government’s total holdings of Citi preferred stock to $52.06 billion.

But before losses mount to the level requiring Treasury to pay up, government officials would gain the power to dictate how the assets are managed. Under the agreement, Citigroup will tap a special CEO from within its ranks to manage the assets, who’ll report to a special internal oversight committee composed of Citigroup’s senior management.

The agreement calls for increased oversight once losses hit $19 billion. At that point, the government can demand “increased reporting, communication or audit requirements,” appoint a government official to sit on the oversight committee, and reduce the compensation of the Citi officials managing the assets.

If losses reach $27 billion, the government can essentially seize management of the assets. The government could tap another company to do the job and “change the fundamental business objective of Citigroup” from “maximizing the long-term value” of the assets to “minimizing losses.” In such a scenario, the government will have effectively seized control of a large portion of Citigroup’s assets (about 15 percent) — a kind of partial nationalization — but only after the bottom falls out.

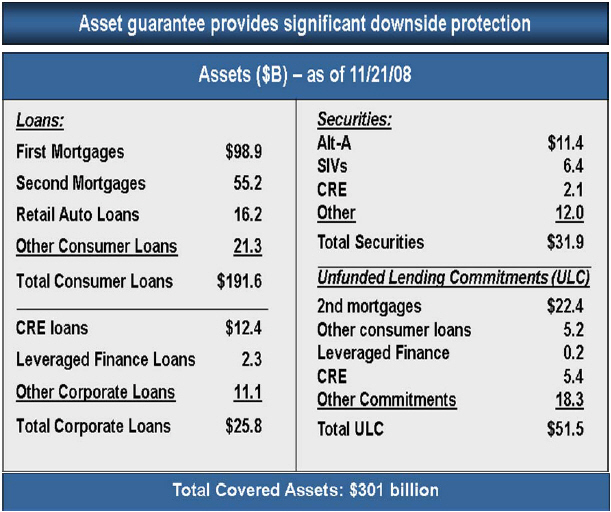

Also revealed in the agreement was more detail concerning the mix of Citigroup assets the government is guaranteeing. According to a chart released by Citigroup, more than half of the assets are residential mortgages, totaling $154.1 billion. Citigroup’s financial statement for the fourth quarter shows Citi held $197.4 billion in mortgages total at the end of the year, meaning that about 78 percent of Citi’s residential real estate loan portfolio is covered by the agreement.

Citigroup’s chart does not detail the credit standards for the loans (whether any are subprime, for instance), only showing that about two-thirds were first mortgages and the remainder second mortgages. We’ve put in a call to Treasury. Meanwhile, a Citigroup spokesman refused to provide more detail.

{kind=link}