Billionaire Peter Thiel, a founder of PayPal, has publicly condemned “confiscatory taxes.” He’s been a major funder of one of the most prominent anti-tax political action committees in the country. And he’s bankrolled a group that promotes building floating nations that would impose no compulsory income taxes.

But Thiel doesn’t need a man-made island to avoid paying taxes. He has something just as effective: a Roth individual retirement account.

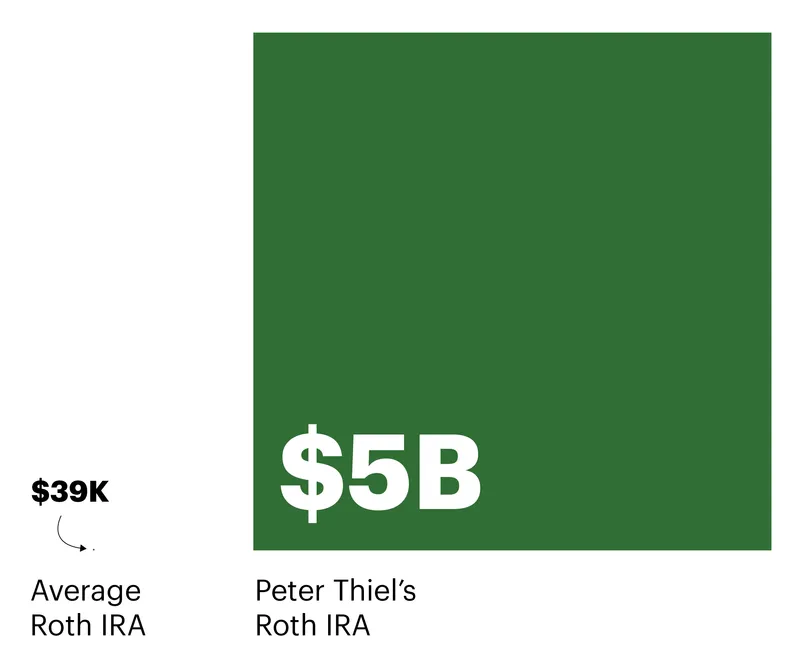

Over the last 20 years, Thiel has quietly turned his Roth IRA — a humdrum retirement vehicle intended to spur Americans to save for their golden years — into a gargantuan tax-exempt piggy bank, confidential Internal Revenue Service data shows. Using stock deals unavailable to most people, Thiel has taken a retirement account worth less than $2,000 in 1999 and spun it into a $5 billion windfall.

To put that into perspective, here’s how much the average Roth was worth at the end of 2018: $39,108.

And here’s how much $5 billion is: If every one of the 2.3 million people in Houston, Texas, were to deposit $2,000 into a bank today, those accounts still wouldn’t equal what Thiel has in his Roth IRA.

What’s more, as long as Thiel waits to withdraw his money until April 2027, when he is six months shy of his 60th birthday, he will never have to pay a penny of tax on those billions.

ProPublica has obtained a trove of IRS tax return data on thousands of the country’s wealthiest people, covering more than 15 years. This data provides, for the first time, an inside look at the financial lives of the richest Americans, those whose stratospheric fortunes put them among history’s wealthiest individuals.

What this secret information reveals is that while most Americans are dutifully paying taxes — chipping in their part to fund the military, highways and safety-net programs — the country’s richest citizens are finding ways to sidestep the tax system.

One of the most surprising of these techniques involves the Roth IRA, which limits most people to contributing just $6,000 each year.

The late Sen. William Roth Jr., a Delaware Republican, pushed through a law establishing the Roth IRA in 1997 to allow “hard-working, middle-class Americans” to stow money away, tax-free, for retirement. The Clinton administration didn’t want to give a fat tax break to wealthy people who were likely to save anyway, so it blocked Americans making more than $110,000 ($160,000 for a couple) per year from using them and capped annual contributions back then at $2,000.

Yet, from the start, a small number of entrepreneurs, like Thiel, made an end run around the rules: Open a Roth with $2,000 or less. Get a sweetheart deal to buy a stake in a startup that has a good chance of one day exploding in value. Pay just fractions of a penny per share, a price low enough to buy huge numbers of shares. Watch as all the gains on that stock — no matter how giant — are shielded from taxes forever, as long as the IRA remains untouched until age 59 and a half. Then use the proceeds, still inside the Roth, to make other investments.

About a decade after the creation of the Roth, Congress made it even easier to turn the accounts into mammoth tax shelters. It allowed everyone — including the very richest Americans — to take money they’d stowed in less favorable traditional retirement accounts and, after paying a one-time tax, shift them to a Roth where their money could grow unchecked by Uncle Sam — a Bermuda-style tax haven right here in the U.S.

To identify those who have amassed fortunes in retirement accounts, ProPublica scoured the tax return data of the ultrawealthy for IRA accounts valued at more than $20 million. Reporters also examined Securities and Exchange Commission filings, court documents and other records, including a memo detailing Thiel’s wealth that was included in his 2005 application for residency in New Zealand.

Among this rarefied group, ProPublica found, the term “individual retirement account” has become a misnomer. Rather than a way to build a nest egg for old age, the accounts have morphed into supercharged investment vehicles subsidized by American taxpayers. Ted Weschler, a deputy of Warren Buffett at Berkshire Hathaway, had $264.4 million in his Roth account at the end of 2018. Hedge fund manager Randall Smith, whose Alden Global Capital has gutted newspapers around the country, had $252.6 million in his.

Buffett, one of the richest men in the world and a vocal supporter of higher taxes on the rich, also is making use of a Roth. At the end of 2018, Buffett had $20.2 million in it. Former Renaissance Technologies hedge fund manager Robert Mercer had $31.5 million in his Roth, the records show.

Buffett didn’t respond to questions sent by email. Mercer couldn’t be reached for comment, and his accountants and attorneys didn’t respond to requests to accept questions on his behalf. Smith also couldn’t be reached for comment, and an employee at his hedge fund repeatedly hung up when ProPublica reporters identified themselves. Other representatives for Smith and his hedge fund didn’t respond.

In a written statement, Weschler said his retirement account relied on publicly traded investments and strategies available to all taxpayers. Nevertheless, he said he supports reforming the system.

“Although I have been an enormous beneficiary of the IRA mechanism, I personally do not feel the tax shield afforded me by my IRA is necessarily good tax policy,” he wrote. “To this end, I am openly supportive of modifying the benefit afforded to retirement accounts once they exceed a certain threshold.”

A spokesman for Thiel accepted detailed questions on Thiel’s behalf, then never responded to phone calls or emails. Messages left at Thiel’s venture capital fund were not returned.

While the scope and scale of such accounts has never been publicly documented, Congress has long been aware of their existence — and the ballooning tax breaks they were garnering for the ultrawealthy. The Government Accountability Office, the investigative arm of Congress, for years has warned that the wealthiest Americans were accumulating massive retirement accounts in ways federal lawmakers never intended.

At the same time, Congress has slashed the IRS’ budget so severely that the agency’s ability to ferret out abuses has been stymied. Money was so tight that at one point in 2015 the agency couldn’t afford to enter critical data about IRAs from paper tax filings into its computer system.

Over the years, a few politicians have tried, and failed, to crack down on the tax breaks the ultrarich receive from their giant IRAs.

In 2016, Sen. Ron Wyden, an Oregon Democrat, floated a detailed reform plan and said, “It’s time to face the fact that our tax code needs a dose of fairness when it comes to retirement savings, and that starts with cracking down on massive Roth IRA accounts built on assets from sweetheart, inside deals.”

“Tax incentives for retirement savings,” he added at the time, “are designed to help people build a nest egg, not a golden egg.”

But Wyden soon abandoned his proposal; there was no chance the Republican-controlled Senate would pass it.

Meanwhile, Thiel’s Roth grew.

And grew.

At the end of 2019, it hit the $5 billion mark, jumping more than $3 billion in just three years’ time — all of it tax-free.

Thiel, a fan of J.R.R. Tolkien, by then had brought his Roth under the auspices of a family trust company called Rivendell Trust. In “The Lord of the Rings,” Rivendell is a secret valley populated by elves, a misty sanctuary against forces of darkness. Thiel’s earthly version resides in a suburban Las Vegas office complex, across from a Cheesecake Factory, and is staffed by a small group of corporate lawyers.

And thanks to the Roth, Thiel’s fortune is far more vast than even experts in tallying the wealth of the rich believed. In 2019, Forbes put Thiel’s total net worth at just $2.3 billion. That was less than half of what his Roth alone was worth.

The ultrawealthy’s hijacking of a tool meant for the middle class becomes especially striking when you consider what the retirement future looks like for many Americans.

There isn’t one.

One in four working-age Americans has nothing saved for retirement, a 2020 Federal Reserve study found.

Individual retirement accounts emerged from the ruins of corporate pensions. The traditional IRA had existed since the 1970s for workers who didn’t have pensions, but as corporations shifted the burden of saving for retirement to workers, too few Americans were setting up these accounts, condemning many to scrape by on Social Security in old age. By the 1990s, politicians on both sides of the aisle were fretting over the declining savings rates in the U.S.

It was against this backdrop that an idea Sen. Roth had been pushing for years finally found its moment.

One of the fathers of Reaganomics, Roth was determined to slash the federal budget, cut taxes and rein in the IRS. Starting in 1997, as chairman of the Senate Finance Committee, Roth held a series of hearings that portrayed IRS agents as menacing thugs. Roth’s investigations sparked legislation that gutted the IRS’ collection powers for more than a decade.

But it was his championing of the Roth IRA that would earn the senator posthumous fame and a mention in the American Heritage dictionary. Roth’s obsession was a new kind of IRA, which he said would “be a blessing to countless Americans as they prepare for the future.”

It would also create an escape hatch from the entire income tax system.

Run-of-the-mill retirement plans — a traditional IRA or 401(k), for instance — defer taxes to a later date. The money that people put into their accounts is deducted from their income, so they aren’t taxed up front, nor are the dividends, interest or gains on investments along the way. But when retirees withdraw money, they have to pay income tax on it.

A Roth, by contrast, eliminates tax liability rather than deferring it. People who open a Roth don’t get the tax break on the money they initially put in. But once they deposit that money, their investments grow tax-free forever and retirees don’t pay a penny of taxes on withdrawals. Even better, unlike a traditional IRA, the Roth doesn’t require retirees to deplete the account as they age.

Sen. Roth promised that his new IRA would “provide relief to hard-working, middle-class Americans.”

The law creating the Roth IRA passed in 1997 with overwhelming bipartisan support. A few tax wonks predicted that workers who were most likely to struggle financially in old age wouldn’t open the accounts because they couldn’t afford to save. Roths, they warned, would become a giveaway to mostly well-off taxpayers who would have saved anyway. Investing in a Roth was like locking in a rate on a mortgage when interest rates were low, an attractive proposition for wealthy Americans worried that Congress would raise tax rates in future years.

That’s why the Clinton administration insisted on barring people who made too much from stashing money in a Roth. Surely, that would prevent the superrich from gaming the system to use Roths as tax shelters.

One day in early 1999, a deputy of Thiel’s at the company that would become PayPal walked into the San Francisco office of Pensco Pension Services. It could have been an uneventful appointment. Instead, it changed Thiel’s life.

Thiel, a Stanford law graduate, ran a small hedge fund and hadn’t yet joined the ranks of the ultrawealthy. But he had outsized ambitions for his months-old tech venture, where he served as both chairman and CEO. He envisioned his company creating “a new world currency, free from all government control.”

Influenced by libertarian Ayn Rand and Tolkien’s fantasy trilogy, Thiel, then in his early 30s, carried himself like a contrarian philosopher king. A few years earlier, he had co-authored a jeremiad against multiculturalism that accused the administration of then-President Bill Clinton of waging class warfare. “Taxing the rich seems to have become an end in itself,” he and his co-author wrote.

Pensco was a small firm that allowed its customers to put nearly any investment they wanted into a tax-advantaged retirement account. Thiel was about to become Pensco’s whale.

In an interview with ProPublica, Pensco founder Tom Anderson recalled how Thiel and other PayPal executives had wanted to put startup shares of the company into traditional IRAs.

Anderson dangled something sweeter.

“I said, ‘If you really think this is going to be big, you know, you might want to consider this new Roth,’” recalled Anderson, who is now retired. If the investment ballooned, he remembered saying, “‘you’re not going to pay tax on it when you take it out.’ It’s a no-brainer."

The math was compelling. Thiel wouldn’t get a tax break up front, but he’d avoid an immense tax bill later on if the investment surged in value.

“They immediately grasped that,” Anderson said. “And they did it.”

What happened next deprived the U.S. government of untold millions in tax revenue. Perhaps billions. Thiel used his new Roth IRA to purchase shares of his startup.

In 1999, single taxpayers were only allowed to contribute to a Roth if they made less than $110,000. Like many startups, PayPal offered its top executives low initial salaries and large stock grants. Thiel’s income that year was $73,263, the IRS records show.

Thiel also had an advantage over most Americans with IRAs, who typically use them to purchase publicly traded stocks, bonds, mutual funds and certificates of deposit. Since Thiel used his Roth to buy shares of a private company, the value wasn’t set on a public stock exchange.

Although the details of such purchases are not usually public, Thiel’s financial assistant later disclosed them in a letter included in the entrepreneur’s application for residency in New Zealand: “Mr. Thiel purchased his founders’ shares in PayPal through his Roth IRA during PayPal’s formation.”

While SEC filings describing that time don’t mention Thiel’s Roth, they show that he bought his first slice of the company in January 1999. Thiel paid $0.001 per share — yes, just a tenth of a penny — for 1.7 million shares. At that price, he was able to buy a large stake for just $1,700.

In 1999, $2,000 was the maximum amount you could put into a Roth in a year.

Thiel’s unusual stock purchase risked running afoul of rules designed to prevent IRAs from becoming illegal tax shelters. Investors aren’t allowed to buy assets for less than their true value through an IRA. The practice is sometimes known as “stuffing” because it gets around the strict limits imposed by Congress on how much money can be put in a Roth.

PayPal later disclosed details about the early history of the company in an SEC filing before its initial public offering. The filing reveals that Thiel’s founders’ shares were among those the company sold to employees at “below fair value.”

Victor Fleischer, a tax law professor at the University of California, Irvine who has written about the valuation of founders’ shares, read the PayPal filings at ProPublica’s request. Buying startup shares at a discounted $0.001 price with a Roth, he asserts, would be indefensible.

“That’s a huge scandal,” Fleischer said, adding, “How greedy can you get?”

Warren Baker, a Seattle tax attorney who specializes in IRAs, said he would advise clients who are top executives working at a startup not to purchase founders’ shares with a Roth to avoid accusations by the IRS that they got a special deal and undervalued the shares. Baker was speaking generally, not about Thiel.

“I would be concerned about the fact that you can’t support the valuation number as being reasonable,” he said.

At the time Thiel bought his founders’ shares, his own hedge fund had already loaned the new startup $100,000, California and SEC records show.

And soon after the company sold him the shares, millions of dollars poured in from investors, securities filings show. In just a month’s time, the company sold a slice of itself to investors for $500,000. That June and August, another $4.5 million poured in from the venture fund arm of telecom giant Nokia and other investors, those records show.

The dot-com boom was in full swing. “We’re definitely on to something big,” Thiel told employees in late 1999, predicting that PayPal would become “the Microsoft of payments,” according to “The PayPal Wars,” a book by a former employee recounting those heady early years.

But when it came time for Pensco, the custodian of Thiel’s Roth, to report the value of the account to the IRS at the close of 1999, none of the investor enthusiasm was apparent. Pensco told the IRS that Thiel’s Roth was worth just $1,664 at the end of 1999, tax records show.

In an interview, Anderson said Pensco relied on the companies whose shares were in a Roth to say what they were worth. He didn’t know how PayPal came up with its market value, but he said Thiel’s purchase of those shares was “very legitimate.”

From there, nothing would stop Thiel’s Roth. In a Silicon Valley equivalent of Tolkien alchemy, his Roth would transform those PayPal shares into a tax-free fortune — one that would be safer than all the gems, gold and silver in the dragon Smaug’s mountain.

After 1999, Thiel would never again contribute money to his Roth, tax records show.

He didn’t need to. In just a year’s time, the value of his Roth jumped from $1,664 to $3.8 million — a 227,490% increase.

Then in 2002, eBay purchased PayPal. That same year, Thiel sold the shares, still inside his Roth, his financial assistant later told New Zealand officials. The tax-free proceeds poured into his account. By the end of 2002, Thiel’s Roth was worth $28.5 million, tax records show.

If he had held his shares outside of the Roth in a normal investment account, Thiel would have owed the IRS 20% of his gains and owed another 9% to California tax authorities. Because the shares were in a Roth, he had no tax bill when he sold them, saving him millions.

Suddenly, Thiel had an advantage few investors could claim: His own personal investment bank that wasn’t subject to taxation. He could now use the cash inside the Roth to buy and sell nearly any investment he wanted. Thiel used the millions in proceeds from his PayPal windfall to invest in other Silicon Valley startups as well as his own hedge fund, according to his financial assistant’s memo. Once again, Thiel’s Roth scooped up startup shares at bargain-basement prices.

For instance, Thiel and colleagues in 2003 founded Palantir, a data analytics company, helped by an early investment from a CIA-backed venture fund. The company was named after the “seeing stones” made by elves in the “Lord of the Rings” trilogy, used to detect danger near and far.

Thiel used his Roth to buy shares of Palantir when it was still a private company, years before it was listed on the New York Stock Exchange, according to a ProPublica analysis of tax records, an SEC filing and shareholder records included in a civil suit.

Over the years, Palantir has won federal contracts from the military to hunt terrorists and from U.S. Immigration and Customs Enforcement to find undocumented immigrants. Even the IRS has a $99 million contract with Palantir to comb through data to identify tax cheats.

Then, in 2004, Thiel met Mark Zuckerberg, a Harvard undergraduate who had come to Silicon Valley for the summer to work on growing the company that would become Facebook. Thiel invested $500,000, Facebook’s first large outside infusion of cash. Those Facebook shares ended up — where else? — in Thiel’s Roth IRA, an attorney for Facebook later disclosed in a letter filed in federal court. That ensured that Thiel wouldn’t owe taxes on his early investment in the company.

As Thiel’s Roth and fortune ballooned, he scolded Americans for their financial imprudence. In a 2006 Forbes column, headlined “Warning: Save, Save, Save,” Thiel lamented the low household savings in the U.S. and called for most Americans to live within their means.

“Forgo the new kitchen and sundeck,” he wrote. “Shoot to put away 15% of the paycheck.” His closing advice: “Living modestly and saving well is better than dying broke.”

In an interview on the website Big Think, Thiel said the U.S. tax system has “fairness problems” in which “you have super rich people paying a lower rate than people in the middle or upper middle class.”

The answer wasn’t taxing the rich more, he said, but “taxing the middle class and the upper middle class a lot less” and cutting their dependence on expensive programs such as Medicare and Social Security.

By then, Thiel had purchased a Ferrari and had bought and sold a penthouse in the San Francisco Four Seasons. In 2005, he sought residency in New Zealand, which had become a destination for some ultrawealthy people who saw it as a safe haven should civilization collapse.

“I have long admired the people, culture, business environment and government of New Zealand, as well as the encouragement which is given to investment, business and trade in New Zealand,” Thiel later wrote in a letter to the country’s government.

Thiel applied as an investor. His application, prepared by his then-financial assistant, Jason Portnoy, touted the size of his Roth. Thiel transferred $749,967 to a bank in New Zealand, keeping it under the umbrella of the Roth.

The country, where the “Lord of the Rings” movies were filmed, approved Thiel’s application. The New Zealand Herald later revealed that the country had secretly granted Thiel full citizenship. The newspaper obtained Thiel’s application through a public records request, and those documents included Portnoy’s letter.

In the next two years, Thiel’s Roth reached new heights, reflecting Facebook’s meteoric rise. In his bestselling book on startups, “Zero to One,” Thiel wrote: “Money makes money.” By the end of 2008, the Roth was worth $870 million.

Up to this point, Thiel was one of the few Americans who had managed to amass prodigious Roth accounts. Among the others were at least three additional PayPal alums who eventually built Roths worth more than $80 million each, according to tax records and SEC filings.

Even so, the existing income limits managed to keep most of the superrich out.

Then, in the latter years of the George W. Bush administration, Congress took a wrecking ball to those defenses, and the wealthy stormed in.

The change centered on an unsexy-sounding maneuver known as a Roth conversion. It works like this: If you have money in a traditional IRA, you can transform it into a Roth as long as you pay one-time income tax on the money. By converting the account to a Roth, no additional income taxes are ever due.

Conversions had existed since the Roth’s conception, but they had been restricted to Americans making below $100,000 per year.

In 2006, Bush and the Republican-controlled Congress were seeking to slash taxes on capital gains, the type of income that can be generated when stocks or other assets are sold. But they faced a problem. Budget rules required them to find a way to make up for the lost revenue.

Their solution was widely viewed as a gimmick: using one tax cut to pay for another tax cut. A provision was included in the Bush bill that lifted the ban on the wealthy making Roth conversions. Since the maneuver requires a payment of tax up front, it counted in short-term congressional budget models as actually raising revenue. The tax breaks didn’t come until later. “It will have large and damaging effects on the federal budget for decades to come,” wrote budget expert Len Burman in the specialty publication Tax Notes.

The new backdoor into the Roth opened in 2010 and set off a frenzy of conversions among hedge fund managers, industrialists and heirs, the tax records reviewed by ProPublica show.

Weschler, the Berkshire Hathaway executive, amassed a giant traditional IRA in his years as a private equity partner and hedge fund manager. He converted a whopping $130 million. His boss, Warren Buffett, converted $11.6 million. After paying the one-time tax, both men saw their Roth accounts soar.

In his statement, Weschler said he opened a retirement account as a 22-year-old junior financial analyst in 1983 and began contributing the maximum amount allowed, along with a generous match from his employer. Weschler said his Roth is so large because he chose investments carefully, had “exceptional luck” and had nearly four decades for it to grow.

Weschler said he could envision the late Sen. Roth holding up his experience as “an aspirational example of the power of deferred consumption” that could “hopefully help motivate generations of future savers.”

He added that he paid more than $28 million in federal taxes to convert his account to a Roth.

Some of the wealthy managed to avoid even that one-time tax bill.

Three members of the Ebrahimi family, whose patriarch made a fortune at the software firm Quark, collectively converted $65 million into Roths in 2010 and 2011. Farhad Ebrahimi, one of the heirs of the fortune, has supported left-wing causes and became known for walking around the Occupy Boston protest in 2011 wearing a hand-lettered T-shirt that declared he was a member of the 1% and said: “Tax me, I’m good for it.”

Kind of.

He converted $19.4 million into a Roth, which would have triggered $6.8 million in income tax. But thanks to losses generated by other investments, he wiped out the tax bill on the conversion. Ebrahimi declined to comment.

In 2009, word of Thiel’s secret weapon leaked for the first time.

In a story headlined, “Give Me Liberty or Give Me Taxpayer Money,” Gawker Media, citing anonymous sources, revealed that Thiel held his Facebook investment in a tax-free Roth.

The Great Recession, though, caught up with Thiel. His hedge fund racked up big losses.

Thiel then did something unusual: For five years starting in 2010, he dipped into his Roth for at least $254 million, the IRS tax return data obtained by ProPublica shows. That is almost unheard of among the wealthy, tax advisers say, because it shrinks the pot of money that can be invested tax-free. Because Thiel was still in his 40s, he was too young to pull money from a Roth without paying income tax plus a 10% penalty on these withdrawals.

During the life of his Roth, Thiel also has made money outside it. He took in an additional $687 million of income from 1999 to 2018, largely from gains on investments, tax records show. All told, over that period he paid $206 million in federal taxes, including the taxes on the early Roth withdrawals.

In four of those years, however, Thiel managed to cut his federal income tax bill to zero.

In 2011, Thiel caught the attention of the IRS. The agency launched an audit, tax records show. The records don’t spell out what the IRS was looking at or if it involved Thiel’s Roth. Whatever the case, the audit was closed years later and Thiel didn’t owe any more taxes, tax records show.

By 2012, large IRAs began to attract scrutiny, falling under the klieg lights of presidential politics.

That January, The Wall Street Journal reported that Mitt Romney, the former private equity executive running for the GOP nomination, had listed on a financial disclosure form that he had amassed an IRA worth between $20 million and $102 million. The story ran on the front page and launched waves of coverage in other publications. Romney had a traditional IRA, not a Roth. But how, people wondered, could the account have grown so large, given that the government imposed strict limits on how much money could be put into one of the tax-deferred accounts?

Citing former company insiders and documents, the Journal reported that during Romney’s time as CEO at investment giant Bain Capital, executives there had effectively bypassed the contribution limits by putting extremely low-valued shares from private equity deals into their IRAs, then watching them balloon.

ProPublica’s analysis of the tax records show that by the end of 2018, at least seven other current or former Bain executives had amassed IRAs worth $25 million or more, with three exceeding $90 million.

Other financiers also found ways to supersize their retirement accounts. Michael Milken, for example, the 1980s junk bond king who went to prison for fraud and was later pardoned by President Donald Trump, had traditional IRAs valued at $509 million.

A senior adviser to Milken declined to answer questions, “since it’s not our practice to publish or discuss Mike Milken’s private financial information, I can’t help you on this one.”

Romney lost the 2012 election, but the IRA revelation provoked a lasting backlash. Wyden asked the investigative arm of Congress to look into the matter. In a landmark report issued in 2014, the Government Accountability Office sounded the alarm, finding the mega IRAs stood “in contrast to Congress’s aim.”

IRS officials told investigators that the federal government was losing more and more money to “IRA abuses.” The GAO investigators flagged “aggressive” valuation tactics by private equity. And while it didn’t mention Thiel or his PayPal co-founders, the report laid out how startup founders’ shares could be used to render IRA contribution limits irrelevant. “Individuals can manipulate contribution limits by grossly undervaluing investments at the time the individual uses an IRA to purchase them,” the congressional investigators wrote.

The report estimated that, as of 2011, there were around 300 taxpayers with IRAs worth more than $25 million. That detail reverberated around the media and Capitol Hill. Few knew that most of those accounts were minuscule compared to Thiel’s, which that year was valued at nearly $1.6 billion.

A series of reform proposals followed. Wyden, who now holds Roth’s old position as chair of the Senate Finance Committee, has become the leading proponent of rolling back what he calls “unfair strategies used by the privileged to rake in subsidies and dodge tax bills with so-called ‘mega Roth IRAs.’” In 2016, he released a plan that would require owners of Roth IRAs worth more than $5 million to take money out of the accounts. Amid howls of protest from the retirement industry and a Senate and House controlled by Republicans, Wyden’s proposal went nowhere.

The IRS, meanwhile, was floundering in its efforts to police retirement accounts. At one point the agency recommended Congress prohibit IRA accounts from buying investments that aren’t traded on a public market, such as founders’ shares. That went nowhere, too. Instead, Congress began slashing the IRS’ budget, kneecapping the agency for more than a decade.

In 2009, an internal team had recommended the agency at least collect data on unorthodox assets held in IRAs. But it took more than five years for the agency to mandate disclosure of those investments. Even then, the agency simply required tax forms to say whether an IRA held stock in a private company, not the name of the company or the price per share.

By 2015, the agency was struggling to handle the paper forms sent in by the companies that administer IRAs. The agency couldn’t afford to digitize them. Another two years went by before the IRS started electronically transcribing the forms.

After years of plodding, the agency said it was finally ready in 2019 to use the data to target potential abusers for audits. And that’s before the real fighting begins over hotly contested issues such as how to value shares in a startup that aren’t publicly traded. IRS officials have complained to congressional investigators that challenging such valuations is costly and time-consuming, and that it requires a small army of experts to go up against deep-pocketed taxpayers.

The IRS did not respond to detailed questions. But as ProPublica has reported, in tax disputes with the superrich, the IRS is completely outmatched.

In his book “Zero to One,” Thiel argues that fortunes are built not by luck or unfair advantage, but by discerning investors and founders who are more courageous than their peers, leaders who zig when the crowd zags. Thiel devotes an entire chapter to the importance of keeping secrets, writing that “every great business is built around a secret that’s hidden from the outside.”

A secret of Thiel’s is that his fortune was built not just with brains but also with massive tax breaks. By 2019, Thiel’s holdings had grown so vast and diverse that his $5 billion was spread across 96 subaccounts inside his Roth.

As his wealth grew, Thiel showered millions of dollars on Republican politicians and groups with an anti-tax agenda, including Club for Growth Action. In 2016, he became the rare Silicon Valley titan to endorse Donald Trump.

The Trump years, which fueled a market boom, were good for Thiel and his Roth. In 2018, he moved his Roth from Pensco to Rivendell, the family trust company named after Tolkien’s elven sanctuary.

In Tolkien’s fantasy world, elves can be killed in battle or succumb to grief, but they don’t die of old age or disease. Thiel has told people he hopes to live to be 120 years old. That might be a bit optimistic, but he is not taking any chances and is investing in anti-aging technology companies. He’s even tucked some of those shares into his Roth, SEC and tax records show.

Assuming a modest 6% annual return and no withdrawals, his tax-free golden egg could be worth about $263 billion in 2087, when Thiel plans to celebrate his 120th birthday. That’s larger than the current gross domestic product of New Zealand, his adopted homeland.

“There is good news and bad news,” Thiel told The Washington Post when asked about living more than a century. “The bad news is: If you don’t believe in the good news, you’re not saving enough for retirement and likely to spend much of your old age in poverty.”

“The financial planning,” Thiel said, “takes on a very different character.”

Paul Kiel, Jeff Ernsthausen and Doris Burke contributed reporting.