One of President Donald Trump’s lesser known but profoundly damaging legacies will be the explosive rise in the national debt that occurred on his watch. The financial burden that he’s inflicted on our government will wreak havoc for decades, saddling our kids and grandkids with debt.

The national debt has risen by almost $7.8 trillion during Trump’s time in office. That’s nearly twice as much as what Americans owe on student loans, car loans, credit cards and every other type of debt other than mortgages, combined, according to data from the Federal Reserve Bank of New York. It amounts to about $23,500 in new federal debt for every person in the country.

The growth in the annual deficit under Trump ranks as the third-biggest increase, relative to the size of the economy, of any U.S. presidential administration, according to a calculation by a leading Washington budget maven, Eugene Steuerle, co-founder of the Urban-Brookings Tax Policy Center. And unlike George W. Bush and Abraham Lincoln, who oversaw the larger relative increases in deficits, Trump did not launch two foreign conflicts or have to pay for a civil war.

The National Debt Increased Under Trump Despite His Promise to Reduce It

Daily total national debt from 2009 to present.

Economists agree that we needed massive deficit spending during the COVID-19 crisis to ward off an economic cataclysm, but federal finances under Trump had become dire even before the pandemic. That happened even though the economy was booming and unemployment was at historically low levels. By the Trump administration’s own description, the pre-pandemic national debt level was already a “crisis” and a “grave threat.”

The combination of Trump’s 2017 tax cut and the lack of any serious spending restraint helped both the deficit and the debt soar. So when the once-in-a-lifetime viral disaster slammed our country and we threw more than $3 trillion into COVID-19-related stimulus, there was no longer any margin for error.

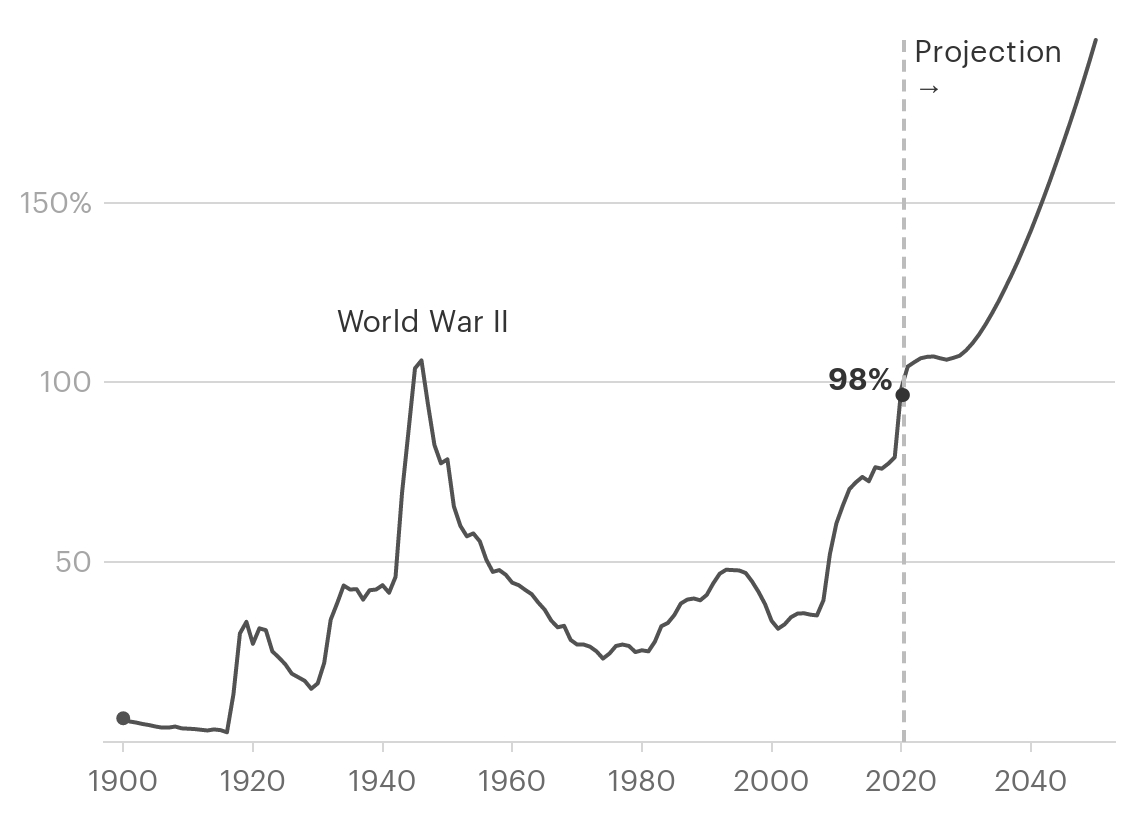

Our national debt has reached immense levels relative to our economy, nearly as high as it was at the end of World War II. But unlike 75 years ago, the massive financial overhang from Medicare and Social Security will make it dramatically more difficult to dig ourselves out of the debt ditch.

The Debt to GDP Ratio Is the Highest It’s Been Since World War II

Federal debt held by the public as a percentage of gross domestic product since 1900.

Falling deeper into the red is the opposite of what Trump, the self-styled “King of Debt,” said would happen if he became president. In a March 31, 2016, interview with Bob Woodward and Robert Costa of The Washington Post, Trump said he could pay down the national debt, then about $19 trillion, “over a period of eight years” by renegotiating trade deals and spurring economic growth.

After he took office, Trump predicted that economic growth created by the 2017 tax cut, combined with the proceeds from the tariffs he imposed on a wide range of goods from numerous countries, would help eliminate the budget deficit and let the U.S. begin to pay down its debt. On July 27, 2018, he told Sean Hannity of Fox News: “We have $21 trillion in debt. When this [the 2017 tax cut] really kicks in, we’ll start paying off that debt like it’s water.”

Nine days later, he tweeted, “Because of Tariffs we will be able to start paying down large amounts of the $21 trillion in debt that has been accumulated, much by the Obama Administration.”

That’s not how it played out. When Trump took office in January 2017, the nonpartisan Congressional Budget Office was projecting that federal budget deficits would be 2% to 3% of our gross domestic product during Trump’s term. Instead, the deficit reached nearly 4% of gross domestic product in 2018 and 4.6% in 2019.

There were multiple culprits. Trump’s tax cuts, especially the sharp reduction in the corporate tax rate to 21% from 35%, took a big bite out of federal revenue. The CBO estimated in 2018 that the tax cut would increase deficits by about $1.9 trillion over 11 years.

Meanwhile, Trump’s claim that increased revenue from the tariffs would help eliminate (or at least reduce) our national debt hasn’t panned out. In 2018, Trump’s administration began hiking tariffs on aluminum, steel and many other products, launching what became a global trade war with China, the European Union and other countries.

The tariffs did bring in additional revenue. In fiscal 2019, they netted about $71 billion, up about $36 billion from President Barack Obama’s last year in office. But although $36 billion is a lot of money, it’s less than 1/750th of the national debt. That $36 billion could have covered a bit more than three weeks of interest on the national debt — that is, had Trump not unilaterally decided to send a chunk of the tariff revenue to farmers affected by his trade wars. Businesses that struggled as a result of the tariffs also paid fewer taxes, offsetting some of the increased tariff revenue.

By early 2019, the national debt had climbed to $22 trillion. Trump’s budget proposal for 2020 called it a “grave threat to our economic and societal prosperity” and asserted that the U.S. was experiencing a “national debt crisis.” However, that same budget proposal included substantial growth in the national debt.

By the end of 2019, the debt had risen to $23.2 trillion and more federal officials were sounding the alarm. “Not since World War II has the country seen deficits during times of low unemployment that are as large as those that we project — nor, in the past century, has it experienced large deficits for as long as we project,” Phillip Swagel, director of the CBO, said in January 2020.

Weeks later, COVID-19 erupted and made the financial situation far worse. As of Dec. 31, 2020, the national debt had jumped to $27.75 trillion, up 39% from $19.95 trillion when Trump was sworn in. The government ended its 2020 fiscal year with the portion of the national debt owed to investors, the metric favored by the CBO, at around 100% of GDP. The CBO had predicted less than a year earlier that it would take until 2030 to reach that approximate level of debt. Including the trillions owed to various governmental trust funds, the total debt is now about 130% of GDP.

Normally, this is where we’d give you Trump’s version of events. But we couldn’t get anyone to give us Trump’s side. Judd Deere, a White House spokesman, referred us to the Office of Management and Budget, which is a branch of the White House.

OMB didn’t respond to our requests. The Treasury directed us to comments made by OMB director Russell Vought in October, in which he predicted that as the pandemic eases and economic growth rebounds, the “fiscal picture” will improve. The OMB blamed legislators for deficits when Trump submitted his proposed 2021 budget: “Unfortunately, the Congress continues to reject any efforts to restrain spending. Instead, they have greatly contributed to the continued ballooning of Federal debt and deficits, putting the Nation’s fiscal future at risk.”

Still, the deficit growth under Trump has been historic. Steuerle, of the Tax Policy Center, has done a comparison of every American president using a metric called the “primary deficit.” It’s defined as the deficit minus interest costs, because interest is the only budget expense that presidents and Congress can’t control unless they want to do the unthinkable and default on the debt. Steuerle examined the records of 45 presidents to see how the primary deficit had shrunk or grown relative to the size of the economy between the first and final years of each president’s administration.

Trump had the third-biggest primary deficit growth, 5.2% of GDP, behind only George W. Bush (11.7%) and Abraham Lincoln (9.4%). Bush, of course, not only passed a big tax cut, as Trump has, but also launched two wars, which greatly inflated the defense budget. Lincoln had to pay for the Civil War. By contrast, Trump’s wars have been almost entirely of the political variety.

Our national debt is now at its highest level relative to our economy since the end of World War II. After the war ended, the extraordinary military expenses disappeared, a postwar recovery began and the debt began to fall rapidly relative to the size of the economy.

But that’s not going to happen this time. When World War II ended 75 years ago, Social Security was in its infancy and Medicare didn’t exist. Today, many of our biggest and most rapidly growing expenses, especially Social Security and Medicare, are baked into the budget because of our nation’s aging population. These outlays are slated to rise sharply. Steuerle recently calculated that Social Security, health care and interest costs are projected to absorb 122% of the total growth in federal revenues from 2019 to 2030.

What’s more, our investment in the future — things like research and development, education, infrastructure, workforce training and such — is declining as a proportion of the budget. OMB data shows that in 1970, mandatory spending (such as Social Security and Medicare, but not including interest on the debt) and investment each made up around 30% of total federal spending. But as of 2019, the most recent available year, mandatory spending had doubled to around 61% of total federal spending while investment fell by more than half, to around 12.5%.

Mandatory Spending Outstrips Investment in the Future

Mandatory and investment spending as a percentage of total U.S. government spending from 1970 to 2019. Mandatory (also known as nondiscretionary) spending includes programs such as Social Security and Medicare, while investment includes infrastructure, research and development, education and training.

Spending more and more on past promises and shrinking the proportion of spending for the future doesn’t bode well for our kids and grandkids. Had Trump done what he said he’d do and paid off part of the national debt before COVID-19 struck rather than adding significantly to the debt, the situation would be considerably less dire. And had Trump done a better job of coping with COVID-19, the economic and human costs would’ve been greatly reduced.

In addition to forcing us to reduce the proportion of the budget spent on the future to help pay for the past, there’s a second reason that huge and growing budget deficits matter: interest costs.

Bigger debt ultimately means bigger interest costs, even in an era when the Federal Reserve has forced down Treasury rates to ultralow levels. The government’s interest cost (including interest paid to government trust funds) was around $523 billion in the 2020 fiscal year. That outstrips all spending on education, employment training, research and social services, Treasury data shows.

Interest costs are way below where they’d be if the Fed hadn’t forced rates down to try to stimulate the economy and mitigate the impact of the pandemic. One-year Treasury securities cost taxpayers a minuscule 0.10% in interest at year-end, down from 1.59% at the end of 2019. The 10-year Treasury rate was 0.93%, down from 1.92%.

In late December, the Fed reported boosting its Treasury holdings by more than $2 trillion from a year earlier. The increase is primarily in longer-term securities. That has kept the federal government from having to raise trillions of dollars in the capital markets, and therefore has kept longer-term interest rates way below where they would otherwise be.

But unless something changes, even the Fed’s promise to keep interest rates near current levels for several years won’t fend off future problems. Most of the government’s borrowing to fund pandemic relief has been shorter-term borrowing that will have to be refinanced in the coming years. If rates rise, so will the government’s interest expense.

Even with rates where they are, interest on the debt is already going to be the fastest-growing budget category this decade, according to the Peter G. Peterson Foundation, which tracks the issue. Annual net interest costs are projected to double in 10 years and grow so large beyond 2030 that interest will become a driving factor in annual deficit growth, according to Peterson estimates.

Listen to what CBO Director Swagel had to say on the subject in a report to congressional Republicans in December: “Although the current low interest rates indicate that the debt is manageable for now and that the United States is not facing an immediate fiscal crisis, in which interest rates abruptly escalated or other disruptions occurred, the risk and potential budgetary consequences of such a crisis become greater over time.”

Trump was asked about this risk during a virtual discussion with the Economic Club of New York last October. “If we have another stimulus bill out of Congress, are you worried that the entire amount of federal debt will be too large for us to pay off in a sensible way?” asked David Rubenstein, a private equity executive.

Trump answered by falsely claiming that the U.S. was starting to pay off the national debt before the pandemic, and he claimed that future economic growth would let it do so. “I think you’re going to see tremendous growth, David, and the growth is going to get it done,” Trump said.

Two months later, when Congress finally approved $900 billion of economic stimulus that is being financed with debt, Trump challenged Congress to spend — and borrow — even more. Then he went golfing.